.jpg)

How Does Bitcoin Work? A Complete Guide for Beginners

Discover how blockchain, nodes, and miners secure the network and enable borderless, 24/7 settlement for your business.

How Does Bitcoin Work? A Complete Guide for Beginners

If you’ve only read about Bitcoin (BTC) in the news but have never tried buying or using it yourself, it may seem like a complicated technology. While it does use sophisticated security features behind the scenes, anyone can gain a basic understanding of how Bitcoin works.

At a basic level, Bitcoin is a digital currency supported by a global network of computers that work together to verify transactions and maintain a shared public record, known as the blockchain. As a foundational part of a multi-trillion-dollar digital asset ecosystem, Bitcoin presents an exciting starting point for understanding how decentralized financial systems operate.

Read on to learn more about how Bitcoin works and what makes it different from traditional payment and monetary systems.

Key Takeaways

- Bitcoin is a digital currency that can be transferred between users using digital wallets.

- Computers around the world use complex algorithms to verify transactions and maintain a shared public ledger.

- Bitcoin’s design prioritizes security through decentralized verification and established best practices for users.

- People gain exposure to Bitcoin by purchasing it directly or investing in cryptocurrency-focused funds or stocks.

How Does Bitcoin Actually Work?

To understand how Bitcoin works, it helps to break it down into a few core components. We’ll cover how you send Bitcoin to people, how transactions are recorded, and how new Bitcoin is created. Together, these pieces explain how Bitcoin operates within the cryptocurrency ecosystem and the broader world.

You Hold Bitcoin Using a “Wallet”

You can’t go to a Bitcoin bank and walk out with physical coins. Instead, Bitcoin ownership is managed through digital wallets. Users manage those wallets with a computer, smartphone, or dedicated hardware devices.

Every wallet consists of a public address and a private key.

The public address is a long string of letters and numbers unique to the wallet. This is the address you provide if you’re receiving Bitcoin or want to check your balance. Anyone with the public address can view the balance and all historical transactions.

The private key is a secret string of letters and numbers used to authorize transactions. Anyone with access to the private key can move the bitcoin associated with that wallet, which is why protecting it is critical.

Wallets generally fall into two categories:

- Hot wallets: These are software-based wallets, such as mobile apps or browser extensions, that are connected to the internet.

- Cold wallets: These store private keys offline, often using dedicated hardware devices or other forms of offline key storage, reducing exposure to online threats.

Bitcoin Moves Directly from Person to Person

Bitcoin allows users to send value directly to one another without relying on banks or other intermediaries.

When someone enters a transaction using their public address and private key, the blockchain network checks that the private key is correct and that sufficient funds are available. If the transaction passes the tests, it’s processed by the network, and the funds are scheduled to move directly from the sending wallet to the receiving wallet.

These peer-to-peer transactions are validated by the network and posted to the public database. Depending on network activity and other factors, transactions are confirmed within a few minutes to a few hours.

The Blockchain Records Everything Publicly

The Bitcoin blockchain serves as a public database containing all transactions since it launched.

The name “blockchain” comes from how the database is structured. When new transactions are submitted, all participating computers work together to ensure they are valid and secure. Verified transactions are bundled into a new group, called a block, and added to the chain of previously created blocks.

Each new block is added to the bottom of the database and can’t ever be reversed or edited.

When a new block of transactions is ready for processing, the computers behind the scenes race to perform complex calculations that secure each transaction and block. When a new block is approved, all those computers receive a copy of it. Each computer has a full copy of the blockchain, so there’s a consensus on which wallets own what Bitcoin.

In some ways, you can think of the entire process like a giant receipt. Everyone who wants to send funds to another wallet submits their transaction to the virtual cashier. The cashier takes those transactions, checks them over, and prints them at the bottom of the receipt. Just like a receipt at any store, it keeps getting longer and longer as more is added to the bottom. But it can’t ever be torn off or changed once printed.

Miners Help Secure the Network

The computers that validate transactions and add new blocks to the blockchain are often called miners.

Of course, mining for Bitcoin is a lot different from the Seven Dwarves mining for gold. Miners play a crucial role in keeping Bitcoin secure by competing to add new transactions to the blockchain. They use powerful computers to perform repeated checks until one of them produces a block that the network will accept. This process is known as proof of work (PoW).

Here’s how miners contribute to the Bitcoin network:

- Miners store a full copy of the public ledger: Miners run software that keeps a full copy of the public blockchain and checks new transactions against the network’s rules.

- Miners compete to perform cryptographic hashing: As new transactions roll in, miners repeatedly run cryptographic checks in an effort to produce a valid block. This trial-and-error process makes it extremely difficult for bad actors to alter transactions or send Bitcoin without the proper keys. This competitive system is what keeps Bitcoin decentralized and tamper-resistant.

- Miners validate new transactions: As all miners participate in validating new transactions, each additional miner adds security to future transactions.

- Miners ensure consensus: As new blocks are approved, they’re shared across the network. Other computers verify it and update their copies of the blockchain. Blocks that don’t follow the rules are automatically rejected.

- Miners earn new Bitcoin: When someone sends Bitcoin, they include a transaction fee paid to the network. The miner that successfully adds a new block earns those fees and, until the total supply cap is reached, a fixed amount of newly created Bitcoin as a block reward.

“Halvings” Ensure a Limited Supply

A core feature of Bitcoin is an event called the halving. About every four years, the network automatically cuts the reward paid to miners in half. This slows the pace at which new Bitcoin is created and released into circulation.

The schedule is fixed in the software and visible to anyone, making Bitcoin’s supply predictable and transparent. Unlike traditional currencies, which can be issued in greater amounts over time, Bitcoin’s issuance steadily declines.

Halvings continue until the total supply reaches its hard cap of 21 million Bitcoin, reinforcing long-term scarcity and supply discipline.

Currently, miners receive 3.125 BTC for being the first to add new blocks to the chain. In 2028, there will be another halving, after which miners will receive 1.5625 BTC as a reward.

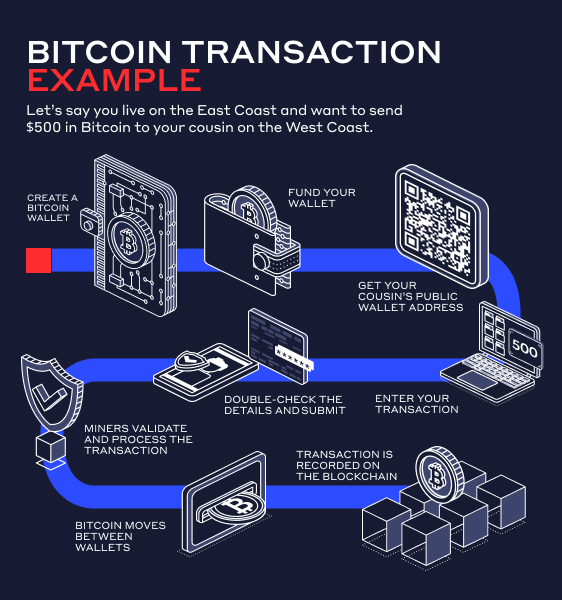

Example: How Bitcoin Transactions Work

To better understand how Bitcoin transactions work, let’s say you live on the East Coast and want to send $500 in Bitcoin to your cousin on the West Coast. Here’s how it would work:

- Create a Bitcoin wallet: The first step is to set up a Bitcoin wallet. Most Bitcoin wallet software allows you to create new addresses for free.

- Fund your wallet: Before sending a transaction, the sending wallet must have enough Bitcoin to cover the amount being sent and the associated transaction fee. How Bitcoin is acquired or funded can vary by platform and jurisdiction.

- Get your cousin’s public wallet address: Now it’s time to get your cousin’s public Bitcoin address. A single typo can mean your currency is lost forever, so double-check that it’s exactly right and verify that it’s the address your cousin wants to use.

- Enter your transaction: Using your wallet software, you’ll enter your transaction details. Your wallet software may automatically fill in some of the details.

- Double-check the details and submit: Make sure the address you’re sending to is correct again, then enter your password or private key and submit the transaction. Transactions are one-way and can’t be reversed once sent to the network.

- Miners validate and process the transaction: Miners receive the transaction and perform their computational magic to ensure it is valid. It’s bundled with other valid transactions and added to the blockchain.

- Bitcoin moves between wallets: Each transaction is assigned a unique transaction ID, and as each miner gets an updated copy of the blockchain, it’s permanently recorded on the public blockchain. The wallet software will automatically display updated balances once enough miners have recorded the transaction.

Now your cousin has the Bitcoin in their wallet. They can hold it there indefinitely, use it to purchase items at retailers that accept BTC, or exchange it back to dollars using a trusted cryptocurrency exchange.

How Does the Bitcoin Network Stay Safe?

Bitcoin is widely regarded as secure because it combines strong cryptography with a network design that makes cheating hard to pull off and easy to spot. Instead of one company running the database, thousands of independent computers keep copies of the same public ledger (the blockchain).

When you send Bitcoin, the network checks that the transaction follows the rules, then records it in a way that becomes harder to change as more blocks are added.

Here are some of the key features that make Bitcoin safe:

- No single point of control: The ledger is shared across many computers, so there is no central server to hack or corrupt.

- Public, verifiable record: Anyone can verify transaction history on the blockchain, making it challenging to hide suspicious activity.

- Digital signatures: Wallets “sign” transactions with private keys, proving the sender is authorized without revealing the key.

- Proof-of-work and mining: Adding new blocks requires significant resources and works well because so many computers contribute.

- Confirmations increase confidence: Each new block added after your transaction makes it progressively more secure and nearly impossible to reverse.

- Rules enforced by software: Network participants automatically reject invalid transactions, such as spending nonexistent coins or double-spending.

Even with a strong network, most real-world losses happen at the device and account level. Keeping your operating system (e.g., Windows, macOS, iOS, Android) up to date helps ensure known security issues are addressed. Turn on automatic updates when possible, and reboot when required to ensure updates apply fully.

Also, keep apps and browsers updated, especially your wallet app and any security-related apps, like password managers and authenticator apps. Use unique, long passwords everywhere, because credential leaks from one site can lead to the same logins being used on another. (A password manager helps make this practical.)

Finally, protect your private keys and seed phrase. Never paste your seed phrase into a website or send it to “support.” Store it offline in a place only you can access. For larger amounts, consider keeping a hardware (“cold”) wallet in a safe.

The Big Picture: A New Future for Money?

While the U.S. dollar remains central to everyday transactions, Bitcoin represents a different approach to money designed for a digital, networked world. Its fixed supply and transparent design set it apart from traditional financial models.

As the first cryptocurrency, Bitcoin has helped define an entire ecosystem and earned comparisons to “digital gold” because of its scarcity and durability over time.

To continue learning about how Bitcoin works—and how American Bitcoin (Nasdaq: ABTC) is helping build the infrastructure behind it—explore our educational resources and stay connected as the ecosystem evolves.

How Does Bitcoin Work? FAQs

- What is a Bitcoin address, and how is it generated?

A Bitcoin address is a unique string of letters and numbers that represents a Bitcoin wallet. You can generate an address using any Bitcoin wallet software.

- What are Bitcoin nodes, and why are they critical for the network?

Bitcoin nodes are computers that store a full copy of the Bitcoin blockchain. They help ensure that all Bitcoin miners and users have access to up-to-date, consistent transaction records.

- How long do Bitcoin transactions take, and what factors affect confirmation time?

Bitcoin transactions take anywhere from a few minutes to a few hours. A higher volume of transactions or a lower number of miners can slow down transaction confirmation, while submitting transactions during low-volume periods can speed up confirmation times.

- Why do Bitcoin transaction fees vary, and who receives them?

Bitcoin fees vary based on network congestion and other factors. Bitcoin miners processing transactions receive transaction fees to compensate for their efforts to secure and maintain the network.

- What is the Bitcoin mempool, and how does it affect pending transactions?

The Bitcoin mempool, short for memory pool, is like a waiting room for transactions. A larger mempool can drive up transaction costs and increase processing times. You can offer to pay a higher fee to get a priority position in line.

- How can businesses integrate Bitcoin payments into their existing systems?

Businesses can integrate Bitcoin into their existing systems through several methods, including using payment providers that instantly convert customer Bitcoin into their local currency or upgrading to accept sales directly in cryptocurrency. You can work with major cryptocurrency exchanges or expert developers to build solutions that accept Bitcoin payments.

- How does Bitcoin enable 24/7, cross-border settlement compared to banks?

Unlike traditional banks, Bitcoin is a 24/7 network that operates worldwide, with no borders or governing entities. It doesn’t matter if you want to send Bitcoin to yourself or use it for an enterprise-scale payment to a partner halfway around the world. The network is always running and ready to process transactions.

Sources

- "What is a Mempool in Crypto?" Trust Wallet. https://trustwallet.com/blog/blockchain/what-is-a-mempool-in-crypto

- "Running A Full Node." Bitcoin.org. https://bitcoin.org/en/full-node

- "How to Invest in Bitcoin and Make Money (Expert Guide 2025)." Koinly. https://koinly.io/blog/how-to-make-money-with-bitcoin/

- "How Does Bitcoin Mining Work? A Beginner's Guide." Investopedia. https://www.investopedia.com/tech/how-does-bitcoin-mining-work/

- "Vocabulary: Hash Rate." Bitcoin.org. https://bitcoin.org/en/vocabulary#hash-rate

- "How Long Bitcoin Transactions Take?" Bitbo. https://bitbo.io/glossary/tx-time/

- "How a Bitcoin transaction works." Trezor. https://trezor.io/learn/supported-assets/bitcoin/how-a-bitcoin-transaction-works

- "Hot vs. Cold Cryptocurrency Wallets: Key Differences Explained." Investopedia. https://www.investopedia.com/hot-wallet-vs-cold-wallet-7098461

- "FAQ: What happens when bitcoins are lost?" Bitcoin.org. https://bitcoin.org/en/faq#what-happens-when-bitcoins-are-lost

- "How does Bitcoin work?" Bitcoin.org. https://bitcoin.org/en/how-it-works

- "Cryptocurrency Prices, Charts and Market Capitalizations." CoinMarketCap. https://coinmarketcap.com/

- "Bitcoin price today, BTC to USD live price, marketcap and chart." CoinMarketCap. https://coinmarketcap.com/currencies/bitcoin/